21/06/23

Essential hedge effectiveness testing: methods and importance

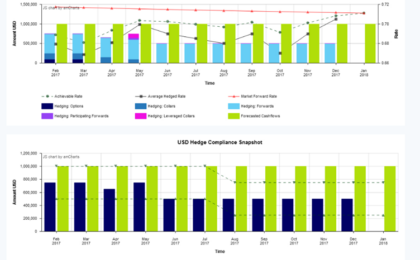

Hedge effectiveness testing is a crucial practice in the world of finance, ensuring the changes in fair value of a hedge adequately offset the changes in fair value of the hedged item. Kevin Mitchell, MD of Hedge Effective Advisory, explores a range of hedge testing methods.

Read more