23/02/24

Year End: Financial Instrument Check List

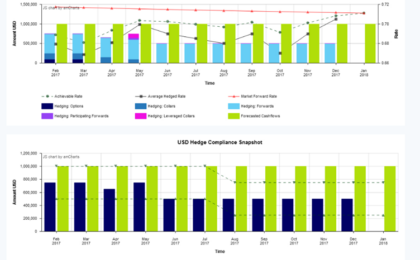

As the end-of-year compliance burden grows for Australian and New Zealand organisations, we put together a practical check list for those exposed to financial instruments such as FX forwards, FX options and interest rate swaps.

Read more